Jim Laszlo, RRC®

Financial Planner, Mortgage Agent Level 1

Financial Planner, Mortgage Agent Level 1

Article Licenses: CA, DL, unknown

Advisor Licenses:

Compliant content provided by Adviceon® Media for educational purposes only.

It is critical to take responsibility and save for retirement

In the information age we are inundated with data, to such a degree, we can get distracted from our principal wealth creation goals. Neuroscientist, Dr. Daniel J. Levitin points out in his book, The Organized Mind, with regard to a never-ending stream of social media, news, and career info, that “our brains are hungrily soaking all this in because that is what they’re designed to do, but at the same time, all this stuff is competing for neuro attentional resources with the things we need to know to live our lives”. And one of the key things we need to know is how to get our finances on track for retirement!

Why people fail to plan A recent article in CNN noted after surveying 1,000 people about retirement that “many people spend more time researching which car to buy or where to go on vacation than they spend on their investments — more than half said they had spent five hours or more doing research the last time they bought a car, and 39% said they spent more than five hours exploring vacation possibilities. Meanwhile, a mere 11% said they had spent that amount of time evaluating investment options”. Levitin makes a case for the need for categorical thinking if we are to wade through the information best suited for our lifestyle. Applying his wisdom, the secret is to determine how you break down your financial strategies categorically speaking, and then determine how you prioritize your processes in relation to your goals. By asking how you organize your finances it forces you to look at and list the most pertinent categories with a realistic application for financial survival:

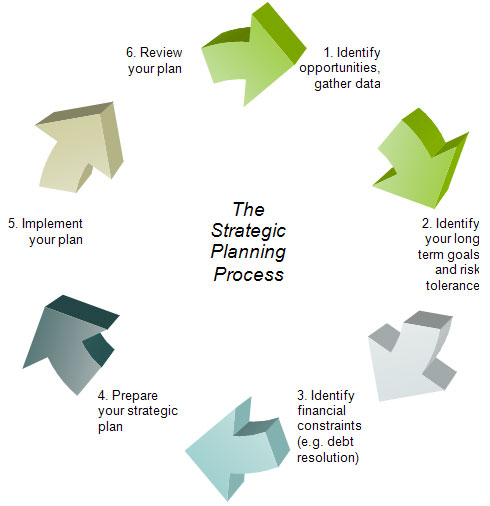

Organize categories as retirement priorities.

There are many factors to consider in the cycle of ongoing, systematic strategic financial organization as you can see in the diagram above. However it is vitally important to apply your powers of concentration to organize strategy in the following key categories, areas within which financial advisors are trained to assist you:

Successful people delegate, so can you

Dr. Levitin points out that “successful people – or people who can afford it – employ layers of people whose job it is to narrow the attentional filter. That is, corporate heads, political leaders, spoiled movie stars, and others whose time and attention are especially valuable have a staff of people around them who are effectively extensions of their own brains, replicating the functions of the prefrontal cortex’s attentional filter”.

In the same way, in order to be successful at retirement planning you may need to engage the help of a professional advisor, someone who often does not charge for his or her services (some advisors are paid via other means), as well as fund specialists and/or investment managers trained to help you achieve financial success.

An advisor can help organize and govern your finances

Again, the logic of The Organized Mind, when applied to finance is simply to get financial guidance – applying the resources of fiscal counsel available. Levitin summarizes this concept of getting someone to handle the daily distractions of life – and unfortunately many view financial organization as a distraction lumped in with all the other media distractions, when it comes down to getting through a basic day, month, or year! Little wonder most people procrastinate when it comes to their finances.

These highly successful persons–let’s call them HSP–have many of the daily distractions of life handled for them, allowing them to devote all of their attention to whatever is immediately before them. Daniel J. Levitan Ph. D. – The Organized Mind -published by Allen Lane

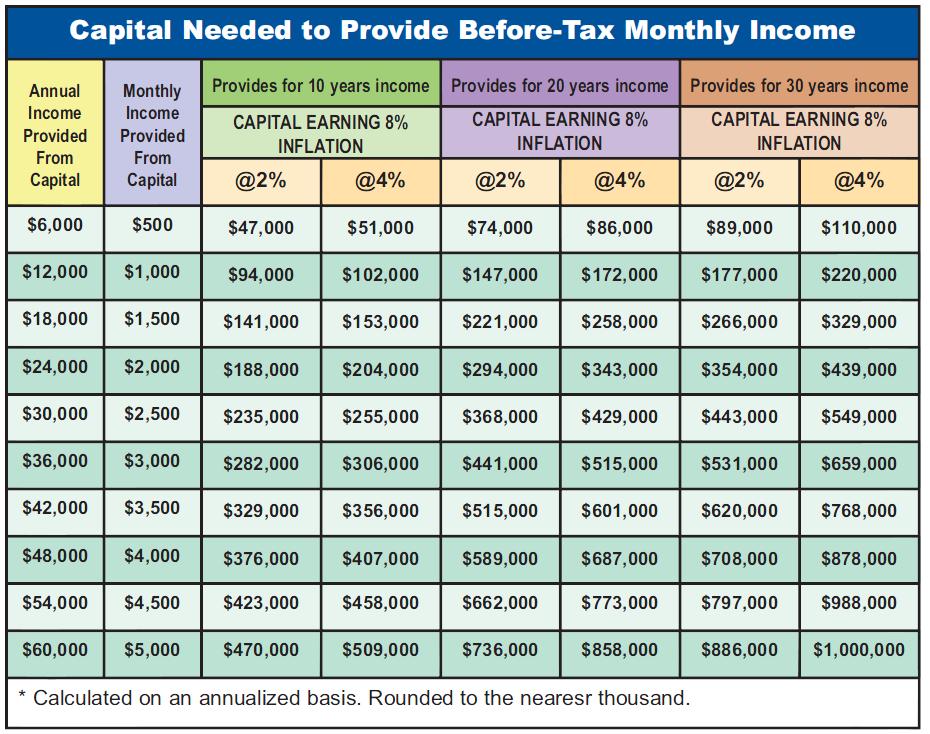

We all want to be successful in our career and workplace as well as in our investment planning. Why not talk to your financial advisor about implementing an organized financial plan – bearing some of the burden to help you get on track – after you study the graph below depicting the capital needed on which to retire. And ask yourself, “is it time that I get help?”

Graph Source: Adviceon

All articles are a legal copyright of Adviceon®Media and are for educational purposes only. The particulars contained herein were obtained from sources which we believe are reliable, but are not guaranteed by us and may be incomplete. This website is not deemed to be used as a solicitation in a jurisdiction where this representative is not registered. This content is not intended to provide specific personalized advice, including, without limitation, investment, insurance, financial, legal, accounting or tax advice; and any reference to facts and data provided are from various sources believed to be reliable, but we cannot guarantee they are complete or accurate; and it is intended primarily for Canadian residents only, and the information contained herein is subject to change without notice. References in this website to third party goods or services should not be regarded as an endorsement, offer or solicitation of these or any goods or services. Always consult an appropriate professional regarding your particular circumstances before making any financial decision. The information provided is general in nature and should not be relied upon as a substitute for advice in any specific situation. The publisher does not guarantee the accuracy and will not be held liable in any way for any error, or omission, or any financial decision.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investment funds, including segregated fund investments. Please read the fund summary information folder prospectus before investing. Mutual Funds and/or Segregated Funds may not be guaranteed, their market value changes daily and past performance is not indicative of future results. The publisher does not guarantee the accuracy and will not be held liable in any way for any error, or omission, or any financial decision. Talk to your advisor before making any financial decision. A description of the key features of the applicable individual variable annuity contract or segregated fund is contained in the Information Folder. Any amount that is allocated to a segregated fund is invested at the risk of the contract holder and may increase or decrease in value. Product features are subject to change.

Life Insurance policies vary according to contract terms. Please read any Life Insurance policy contract provided, or the segregated fund summary information folder prospectus before the time of purchase. Full details of coverage, including limitations and exclusions that apply, are set out in the policy of insurance. Commissions, trailing commissions, management fees and expenses may be associated with segregated fund investments which may not be guaranteed and their market value changes daily and past performance is not indicative of future results. A description of the key features of a life insurance policy, a segregated fund; and any applicable individual variable annuity contract is contained in information provided by the company from which it is purchased. Talk to your advisor before making any financial decision. For specific situations, advice should be obtained from the appropriate legal, accounting, tax or other professional advisors. The information provided is accurate to the best of our knowledge as of the date of publication and is general in nature, intended for educational purposes only, and should not be relied upon as a substitute for advice in any specific situation. For specific situations, advice should be obtained from the appropriate legal, accounting, tax or other professional advisors. Rules and their interpretation may change, affecting the accuracy of the information.